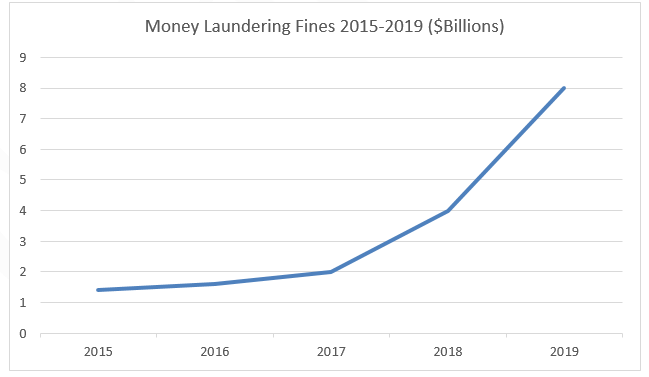

The focus of banks and other financial institutions on enhancing their anti-money laundering (AML) setups has never been higher. The substantial increase in the number and magnitude of fines issued by market regulators (which have grown from $4B in 2018 to above $10B in 2020), as well as the release of record fines of above $1B to individual players, makes revisiting financial crime processes a must-do for all financial players.

But this task is far from simple. AML is a complex issue which can take multiple forms and shapes and impact different key processes within financial players. Financial crime mechanisms also tend to evolve extremely quickly as offenders find new ways of developing AML strategies, tax evasion, and more. Leveraging data across processes within a financial institution as well as across financial players becomes a requirement when taking up the challenge.

The different shape and forms of financial crime

Although banks and other financial players are required to review their AML risk frameworks to meet compliance and regulatory obligations, it is also an important area of potential cost reduction or management. The whole industry is striving to shift spending from risk framework reinforcement to customer-focused investments, which requires players to revisit their ways of approaching complex risk topics such as financial crime management and boost risk/return of their strategies.

Enhancing AML Setups: It's More Than Just Machine Learning

When revisiting their AML setups, most financial players tend to face similar challenges across the AML value chain:

Efficient AML Starts at the Know Your Customer (KYC) Level

This step is all the more complex in the institutional space, as it demands analysis of companies and counterparts across a broad range of dimensions to validate suitability of new business relationships. It is thus absolutely critical to get right for organizations as the first protection against being exposed to money laundering, terrorism financing, or other financial crime activities.

Traditionally in KYC, analysts collect documents and information, analyze them, and make a judgement call on the level of risk represented by a given individual or company. But doing so can be a tedious effort, which can be greatly reduced thanks to data science, via e.g., leveraging broad sets of signals built from traditional, alternative, and public data; understanding these through graph analysis; and leveraging Optical Character Recognition (OCR) and Natural Language Processing (NLP) to enhance processes automation. This reduction of tedious or lower value effort in turn enables KYC analysts to significantly reinforce the accuracy of their reviews as well as reduce the time taken by individual investigations.

Once Established as a Customer, AML Becomes a Day-to-Day Task

In banks, all types of transactions and requests are tightly monitored to identify anomalies, patterns, and connections leading to additional risk or suspicious activity. This creates a new set of needs:

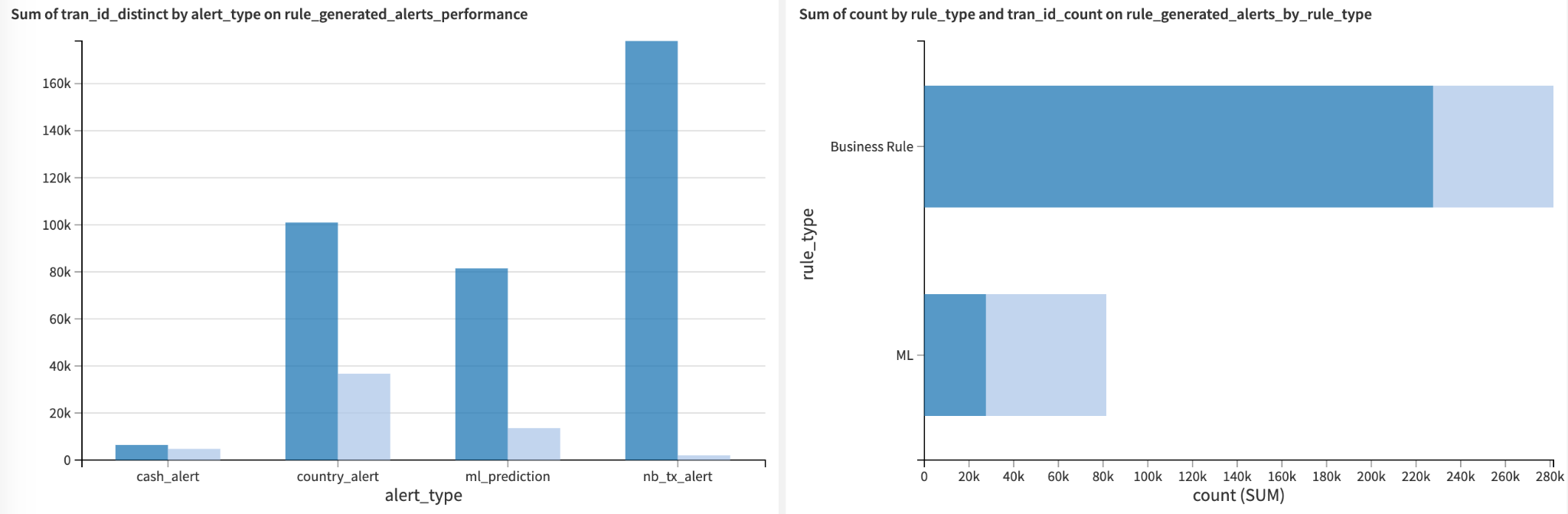

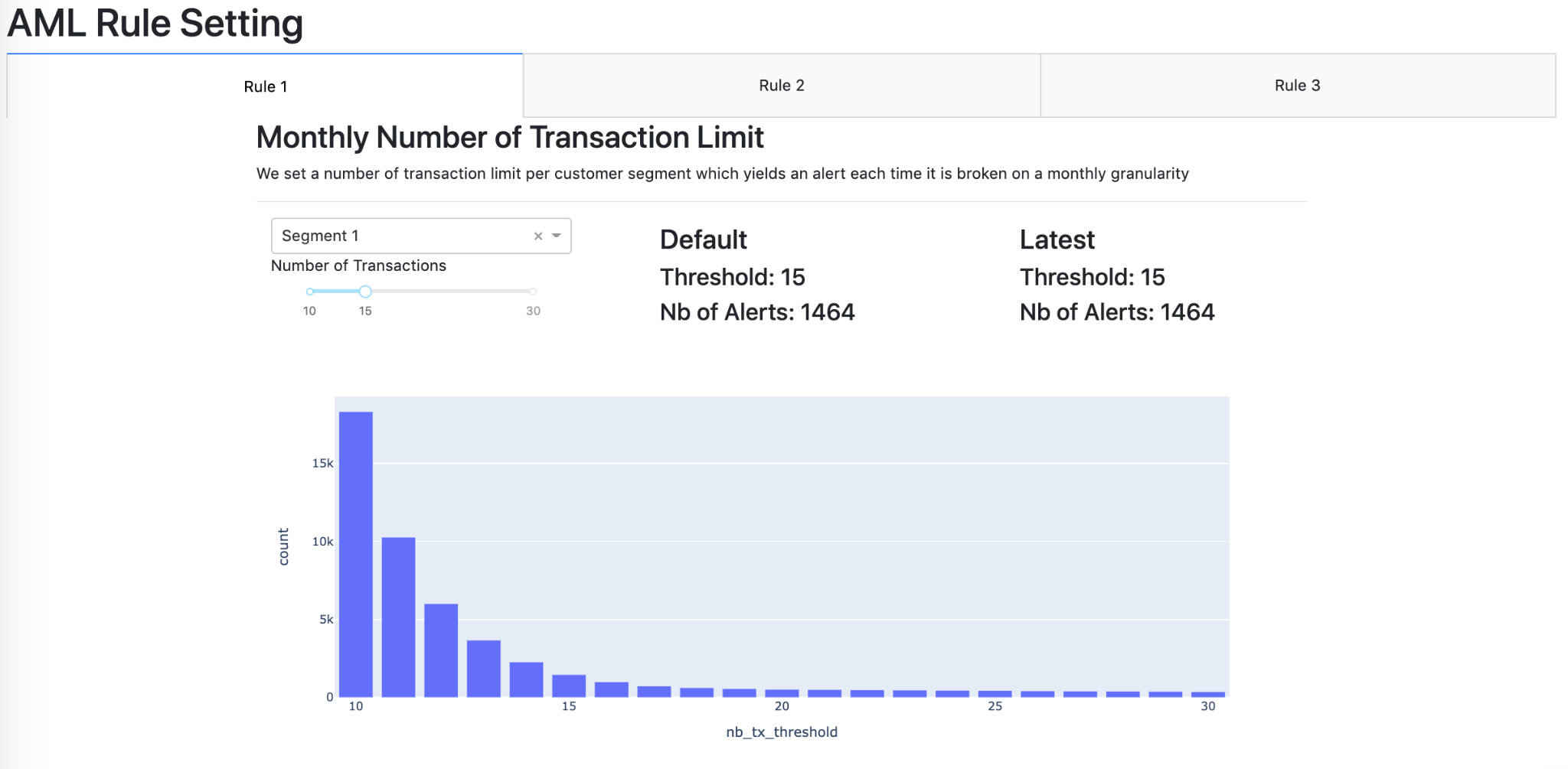

1. Easily test and roll out new alerts, ranging from traditional, rules-based ones (i.e., a specific threshold being hit on cash withdrawal) to machine learning (ML) and graph-powered ones:

Dataiku dashboard comparing rules-based and ML-based alerts

For financial institutions, the name of the game is to find the unique capacity to mix agility and robustness: agility is needed in testing new thresholds and tailoring alerts to specific populations and activities (by geography, by branch, etc.), for quickly moving from sandbox to production., and for quickly engaging risk management and other control teams in the validation of resulting changes. This agility needs to be combined with the highest levels of robustness when it comes to auditability, documentation, and guaranteeing optimized operationalization.

For banks and other financial institutions, the benefits of data science are thus clear: ML can bring a step change in the capacity to develop new types of alerts, be it through initial clustering or identification of patterns. Combining these with graphs can further enhance ways to identify unique patterns. As financial players embark on this trajectory, they will need to be able to constantly demonstrate their capacity to navigate between the different approaches and fully own them, with the highest standards of explainability so as to comply with regulatory requirements (see, as an example, the demands from ACPR).

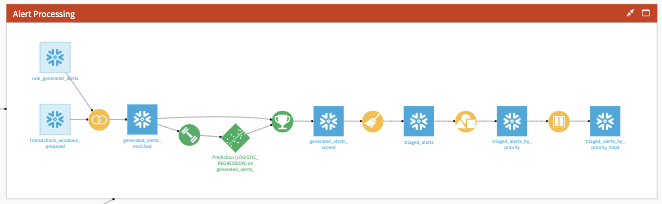

2. From tiering alerts to reducing false positives:

In order to maximize the efficiency of their setups, banks and other financial institutions constantly strive to ensure they prioritize their investigation efforts. This can happen at two distinct moments in the AML process. The first is post-integration in AML case management systems. Once in case management systems, it becomes mandatory for financial institutions to treat all alerts in due time, leading to a review by an investigator and decision to file a report to national regulators (or not).

As part of this effort, ML can be applied to support alert tiering, thus helping prioritize alerts and give early indication on the intensity of investigation likely to be required. Such an approach combined with formal tracking of outputs can, in turn, be used to revisit active alerts in a much more agile, analytics-powered approach.

The second is pre-integration in AML case management systems, with the objective of reducing false positives. Thanks to the above and leveraging results of past investigations, ML models can be applied earlier in the process to reduce volumes of alerts.

3. Reducing time spent and augmenting accuracy of investigations:

After alerts are raised, it’s time for investigation. We have discussed above how ML supports improved tiering and false positive reduction, as well as agile revisiting of alert generating models over time. The potential of data science for AML does not stop there: analytics and, most notably, graph analytics can bring a step change to the efficiency of the work of investigators, with the potential to reduce time for investigation by two to three. Developing process automation on fact finding per types of alerts can also greatly speed time-to-management of the different generated alerts.

Collaboration Between Data Scientists, IT, and AML Specialists Is Instrumental

The enhancements described above are well known to the compliance community. Most teams are engaged in active work to revisit their approaches, aiming to find the right balance between preserving setups capable of passing regulatory checks and exploring the potential of data science to enhance. The question for banks and financial institutions is not on why or what, but on how to bring this change.

If we were to formulate some recommendations, the first is that it is a journey involving multiple players. AML is a highly regulated environment with every growing scrutiny from regulators. As the institutions guarantee the robustness of the financial systems and the fair treatment of all customers, it is paramount to them to ensure all AML setups are well sized and owned. Introducing data science in AML should thus be seen as a step-by-step journey which will take compliance leads from traditional rules-based and processes to AI-enhanced ones, leveraging the full spectrum of data science — and ensuring all stakeholders bring AI to their everyday activities, from KYC and alerts generation to investigation.

To do so, building strong collaboration between data science experts and compliance leads is a requirement, alongside efficient and agile processes with IT so as to be in a position to promptly enhance a set of models. Strong collaboration is also key to guaranteeing advanced levels of explainability and thus enabling compliance managers to pass any internal or external audit on models used.

We have by now seen why this transformation project, standing at the top of all banks and financial institutions’ strategic agendas, is a complex one to perform. Thanks to its unique capacity to bring data scientists, compliance officers, IT and more in a collaborative environment, Dataiku’s central analytics platform can support financial organizations to bring a step change to such projects by providing:

1. A unified environment to develop the full scope of analytics and data science models required by AML.

From NLP and ML to graph analytics, Dataiku users can leverage a mix of built-in processors, visual ML, and coding environments to develop fit-for-purpose data projects.

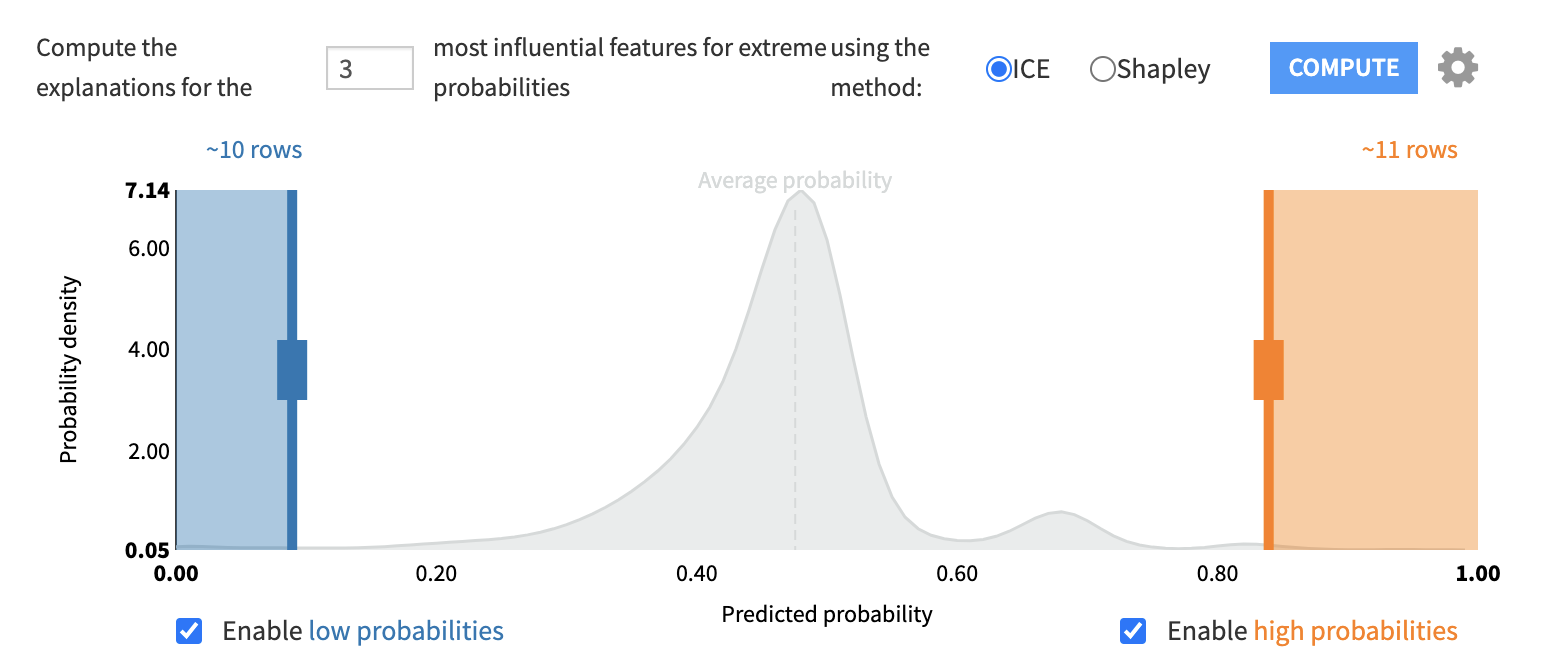

2. A full set of explainability features to guarantee understanding of ML models by compliance leads and auditing parties.

3. The capacity to develop custom visualization dashboards and webapps to ease alert design and monitoring.

{kind=link}

4. Full, eased integration with the full ecosystem, from data inputs and case managers to graph analytics visualization tools.

While enhancing AML is a journey, it can be accelerated by empowering teams to develop their AI-enhanced processes, thus guaranteeing full ownership and capacity to make these evolve as the AML landscape continues to.