Estimating risk is the essential ingredient to determine the price of an insurance policy. The estimated risk of an insurance policy is the minimum price an insurer should quote to be breakeven, therefore evaluating this risk with precision and confidence is the foundation of a robust quoting system. For decades, actuaries have used statistical models to predict the risk of losses or damages to calculate an insurance price. Since the 1980s, the type of model used to do it has evolved. It is now a common approach to consumer insurance claims modeling across the world to use Generalized Linear Models (GLM). This type of modeling has a deep, rich, and proven track record.

GLM are a generalization of the linear regression and they combine the interpretability and simplicity of linear models while allowing for more flexibility thanks to the choice of the link function and the target distribution. Some phenomena of major importance for actuaries exhibit behaviors that do not fit the assumptions of the standard linear regression. Two examples are the claim frequency (the number of claims filed by a policyholder over a given period of time) which is a counting process usually modeled with a Poisson distribution, or the claim severity (the claim amount for a given claim) which is often modeled using a Gamma distribution.

Although GLM models have changed the way actuaries work, a lot of existing GLM solutions are often outdated and require complex and potentially unreliable nests of supporting systems to work effectively — starting with limited capabilities on data ingestion and API development. It often is too rooted in outdated systems that it fails to welcome new techniques and improvements.

GLM and Data Science

With the goal of both taking advantage of current data science techniques and improving the efficiency of actuary teams, GLM models can be brought into a more modern setup. But how can organizations do so?

Mainly, they can make sure the value of approved GLMs techniques is retained while dramatically improving the efficiency and effectiveness of their teams developing them. The setup on which this happens needs to include modern data science capabilities while also respecting the rules of governance that the work of actuaries might be subject to.

That’s where Dataiku’s latest released solution offers an answer. Its goal is to:

- Enhance upstream and downstream processes, including data wrangling and API connectivity.

- Easily improve existing workflows or pricing modules incrementally with machine learning, as and when desired.

- Establish effective governance, analytic best practices, and centralization of pricing workflows, without sacrificing agility.

Embarking on this journey acts as a foundational step towards developing innovative insurance pricing strategies, enabling to significantly improve the efficiency of actuaries teams.

How Can Dataiku's Business Solutions Help You Reach Full Potential?

Business Solutions are Dataiku add-ons accelerating the way to achieve advanced or foundational industry-specific use cases within your organization. They are an operational shortcut to achieve real-world business value. Taking advantage of Dataiku’s core features, they are built to be fully customizable and entirely editable.

They come with:

- A user-friendly interface that enables fine tuning to match specific business requirements

- Ready-to-use dashboards that can be customized

- Documentation and training materials

Dataiku industry specialists develop solutions for every vertical, among which:

- Retail & CPG: Distribution spatial footprint, market basket analysis, RFM-enhanced customer lifetime value, product recommendation

- Financial services and insurance: Interactive document intelligence for ESG, modern insurance pricing, AML alerts triage

- Health and pharmaceuticals: Omnichannel marketing, accelerating drug repurposing

- Manufacturing and energy: Predictive maintenance, outliers detection

As a result, business professionals experience a boost in AI productivity and can rationalize their resources.

How Does It Work in Practice?

The Insurance Claims Modeling with GLM solution provides a reusable project to modernize the use and practice of GLM models.

With this solution, actuaries, pricing product teams, or claims models reviewers will be able to:

- Easily develop GLM-based risk pricing by designing complete workflows within Dataiku’s no-code VisualML environment.

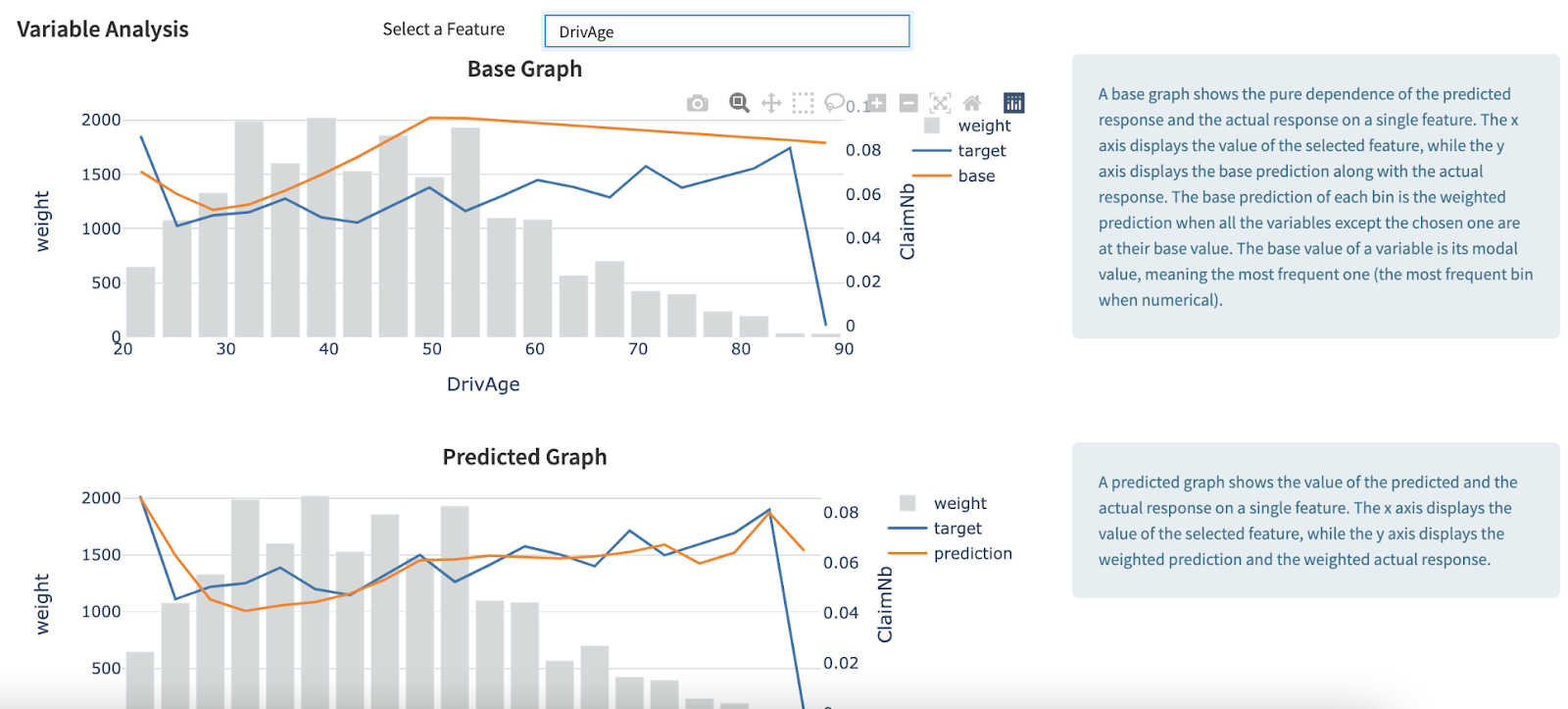

- Rapidly develop detailed analytic insights using powerful exploratory data tools, entirely within Dataiku.

- Ensure comprehensive governance and controls with a centralized space for common datasets, tracked changes, and comprehensive model and process review.

- Enable real-time scoring by easily deploying finalized models for use in other systems internally or externally.

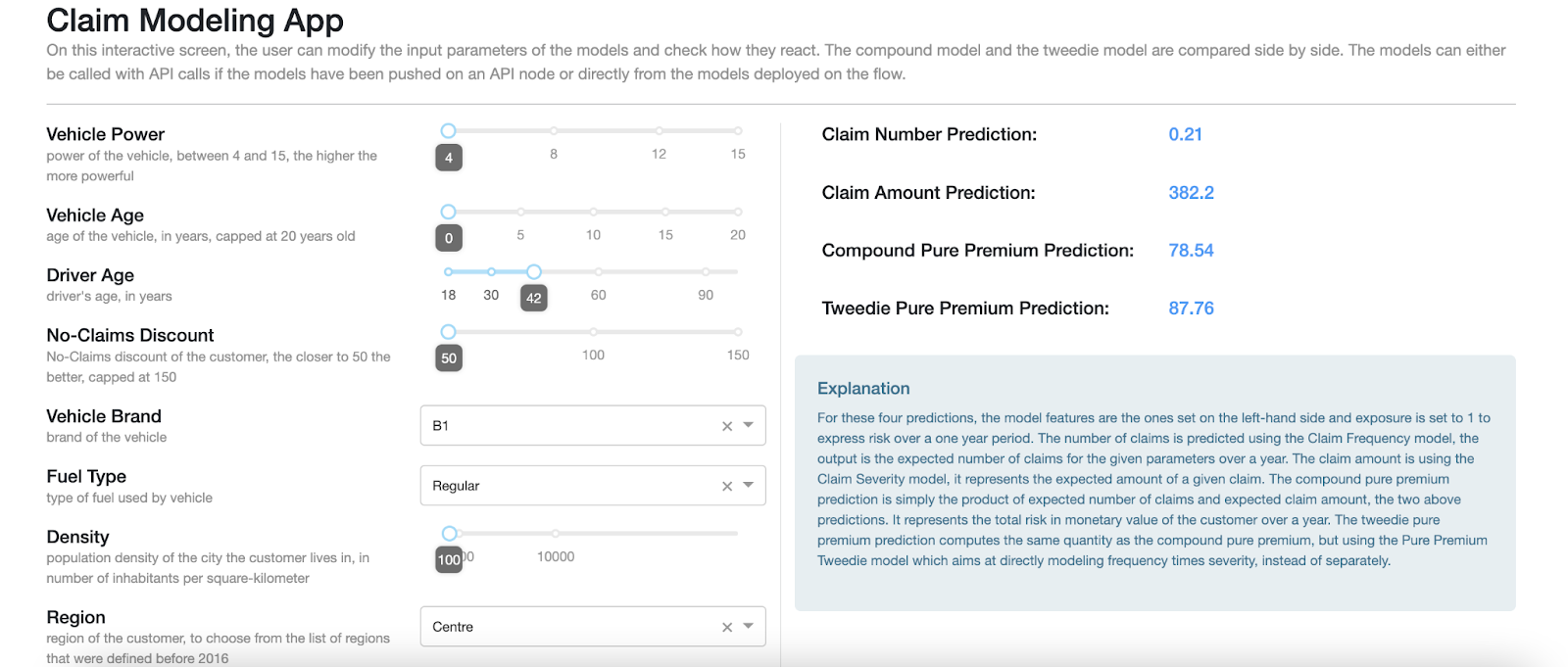

- Develop real-time experimentation on model results using the powerful and interactive modeling application.

From a user perspective, the solution is made of the following easy-to-use components:

1. Easy and Powerful Data Wrangling and Feature Generation

Easily iterate across large amounts of data, exploring meaningful relationships and identifying potentially powerful interactions.

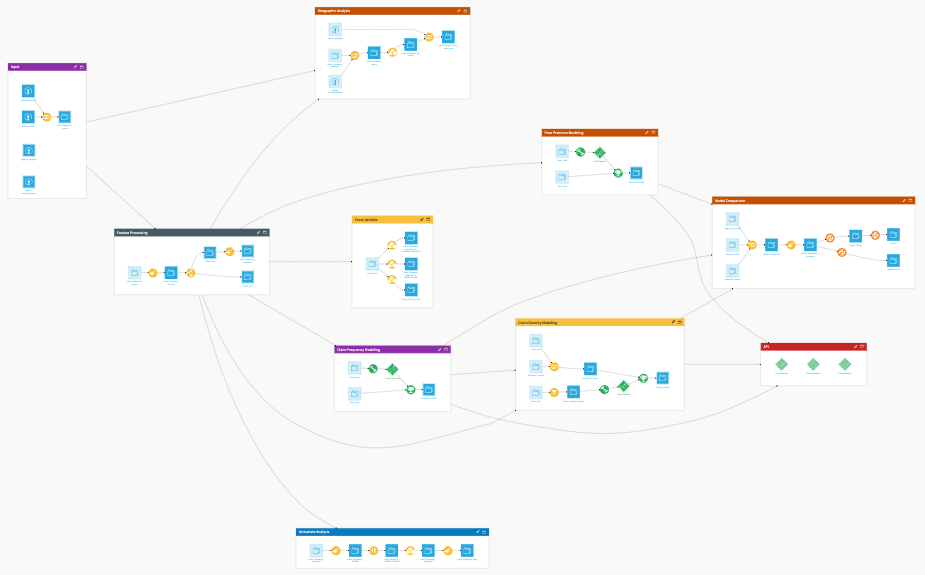

2. Visual Pipeline

Get a clear and simple understanding of the project structure and data transformation steps. Dataiku offers simple navigation, modification, and oversight of the project.

3. Powerful Visual GLM Features

Develop complete and powerful GLMs entirely within the Dataiku platform, and ensure all supporting steps (data loading and transformation) and outputs (API, models) are directly connected and easily reviewed or modified.

4. Powerful and Easy-to-Use Apps

The interactive application allows for real-time experimentation on model results based on changes to feature values and for simple ‘what if’ analysis.

{kind=link}

Start modernize your GLM activities right now, with these simple requirements:

- Datasets: Historical claims

- Dataiku version: 10.0 or later